Government and industry representatives met on the 6th October 2025 for the most recent International Nickel Study Group meetings, during which the Group reviewed its forecasts for nickel production and use in 2025 and 2026. This article gives a brief overview of recent developments and is based on the data finalised at the meetings.

By Ricardo Ferreira, Director of Market Research and Statistics & Francisco Pinto, Manager of Statistical Analysis, International Nickel Study Group (INSG)

Global economic growth proved stronger than anticipated in early 2025, supported by increased investment in artificial intelligence–related activities in the United States, fiscal stimulus measures in China, and a temporary acceleration of trade flows ahead of expected tariff increases.

Nonetheless, the pace of expansion is projected to moderate in 2026. Looking forward, the introduction of higher tariffs may have implications for global trade, investment decisions, labour markets, and price dynamics. On a more favourable note, financial conditions have eased, and inflation is expected to decline across the majority of G20 economies.

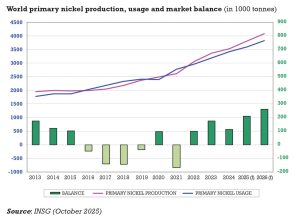

During its October 2025 meetings, the International Nickel Study Group (INSG) revised its forecast for the 2025 nickel market balance, projecting a surplus of 209 thousand tonnes (kt). Primary nickel production in 2025 is estimated at 3.81 million tonnes (Mt), while usage is expected to reach 3.60 Mt. Preliminary projections for 2026 also indicate a surplus, estimated at 261 kt, with production forecast to rise to 4.08 Mt and usage to 3.82 Mt.

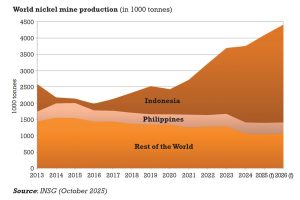

Nickel mine production

World nickel mine production grew by 1.8% in 2024 and is projected to rise by a further 8.9% in 2025 and 7.8% in 2026. Indonesia remains by far the world’s largest mine producer, accounting for an estimated 66% of global output in 2025, with its share projected to rise to around 68% in 2026. The country’s robust production growth continues to be driven largely by Chinese-backed projects, which are rapidly expanding processing capacity both for intermediate products – such as nickel matte and mixed hydroxide precipitate – and for primary products, including nickel pig iron (NPI), nickel sulphate, and nickel cathode.

World nickel mine production grew by 1.8% in 2024 and is projected to rise by a further 8.9% in 2025 and 7.8% in 2026. Indonesia remains by far the world’s largest mine producer, accounting for an estimated 66% of global output in 2025, with its share projected to rise to around 68% in 2026. The country’s robust production growth continues to be driven largely by Chinese-backed projects, which are rapidly expanding processing capacity both for intermediate products – such as nickel matte and mixed hydroxide precipitate – and for primary products, including nickel pig iron (NPI), nickel sulphate, and nickel cathode.

Primary nickel production

World primary nickel production is projected to increase by 7.9% in 2025, following a 4.9% rise in 2024, with further growth of 7.2% expected in 2026. In Asia, output is forecast to reach 3.11 Mt in 2025 (+9.4%) and 3.37 Mt in 2026 (+8.1%). Despite Indonesia’s recent efforts to tighten control over its mining sector – including delays in the issuance of mining permits (RKABs), land seizures due to missing forestry approvals, and sanctions related to insufficient reclamation or post-mining guarantees – the effects on nickel feed supply have so far been temporary or limited.

World primary nickel production is projected to increase by 7.9% in 2025, following a 4.9% rise in 2024, with further growth of 7.2% expected in 2026. In Asia, output is forecast to reach 3.11 Mt in 2025 (+9.4%) and 3.37 Mt in 2026 (+8.1%). Despite Indonesia’s recent efforts to tighten control over its mining sector – including delays in the issuance of mining permits (RKABs), land seizures due to missing forestry approvals, and sanctions related to insufficient reclamation or post-mining guarantees – the effects on nickel feed supply have so far been temporary or limited.

As a result, production of various nickel products is anticipated to continue expanding in both 2025 and 2026.

Indonesia, the world’s leading primary nickel producer since 2021, is forecast to raise output to 1.9 Mt in 2025 and 2.1 Mt in 2026, further consolidating its dominant position. By 2026, the country is expected to account for around 51.4% of world primary nickel output, reflecting its pivotal role in global supply growth. Production gains will be supported by rising output of NPI as well as nickel sulphate and nickel cathode, of which the latter two began production domestically in 2023. The majority of the output is intended for export.

China (P.R.), the world’s second-largest producer, is projected to account for 26.9% of global production in 2026. The ongoing shift from declining NPI production toward higher cathode output is expected to persist. While nickel sulphate production is projected to moderate in 2025 amid softer battery demand, although a rebound is anticipated in 2026.

Combined Chinese and Indonesian NPI output is forecast to reach 2.05 Mt in 2025 and 2.17 Mt in 2026, underscoring the two countries’ central role in global nickel supply growth. Overall, most of the expansion in world primary nickel production in 2026 is expected to take place in Asia.

In other regions, profitability challenges have led several facilities to suspend operations, curtail output, or consider future shutdowns. As a result, all regions outside Asia recorded declines in primary nickel production in 2024. The Americas are forecast to recover in 2025 and 2026, with output expected to rise by 11.2% and 6.1%, respectively, supported by higher production in Brazil and Canada. In contrast, both Africa and Europe are projected to see further declines in 2025 (-4.4% and -1.1%, respectively) before returning to growth in 2026 (+10.1% and +0.5%). Oceania’s production is anticipated to drop sharply again in 2025 (-39.4%) and then stabilise in 2026.

")

Primary nickel usage

Global nickel usage has expanded steadily since 2009, with the sole exception of 2020, when consumption declined marginally by 0.6%. In the short term, usage is forecast to grow by 5.3% in 2025 and a further 6.2% in 2026, with China contributing most of the increase in absolute terms in both years.

Asia’s dominance in the nickel market will continue to strengthen, accounting for 87.7% of global primary nickel usage in 2025 and 88.2% in 2026. For comparison, the region’s share stood at 63% in 2010.

In China, primary nickel demand is expected to rise by 6.8% in 2025 and 6.4% in 2026. The country remains by far the largest consumer and will account for more than 65% of global primary nickel usage in both years. Demand continues to be driven mainly by developments in the stainless steel (STS) sector. Although the battery sector’s contribution is projected to ease slightly in 2025, its growth momentum is expected to strengthen again in 2026.

Indonesia, which began producing stainless steel in 2017, became the world’s second-largest nickel consumer in 2020, surpassing Japan. Following rapid growth in 2021, when demand reached 383 kt, consumption fell in 2022 and 2023 due to import restrictions on STS imposed by several countries. It rebounded in 2024 and is projected to increase by 4.8% in 2025 and a strong 14.5% in 2026. From 2025 onwards, Indonesia will also begin using nickel in the production of electric vehicle (EV) batteries, as part of its broader objective of developing a downstream battery and EV industry.

In Europe, nickel usage declined in 2024 and is expected to fall further in 2025 (-0.5%) before recovering modestly in 2026 (+1.8%). Persistent economic challenges and labour disruptions in some stainless steel mills have weighed on regional demand in recent years.

In the Americas, consumption is forecast to rise by 4.6% in 2025 and 0.9% in 2026, led by the United States, where demand is projected to grow by 5.2% in 2025 and 0.8% in 2026.

African nickel usage is anticipated to decline by 4.8% in 2025 before rebounding sharply by 26.3% in 2026. A new battery plant began operations in Morocco in 2025 and is set to stimulate regional demand in the following years. Globally, the STS sector remains the dominant first-use market for primary nickel, currently accounting for just under 70% of total consumption. In contrast, nickel use in EV batteries declined slightly in 2025, reflecting the withdrawal of government subsidies, growing competition from non-nickel chemistries – particularly lithium iron phosphate (LFP) – and a shift in consumer preference from battery electric vehicles (BEVs) towards plug-in hybrid electric vehicles (PHEVs). Despite this temporary setback, demand for nickel in the battery sector is projected to resume growth in the coming years.

Capacity and new projects

In its 2025 edition of the World Directory of Nickel Production Facilities, the INSG reported a total of 565 operating nickel mines across 31 countries and 273 operating smelters and refineries in 32 countries.

Global primary nickel capacity was estimated at 5.49 Mt. Based on 2024 data, approximately 64% of that capacity was in operation. The People’s Republic of China had the largest installed capacity at 2.17 Mt, followed by Indonesia with 1.78 Mt.

Regarding new developments, the directory identified 178 committed projects (including projects that have started and are ramping up) in 16 countries, along with 60 likely and 146 potential projects spread across 16 and 27 countries, respectively.

New capacity from committed projects was estimated at 447 kt of ore/concentrate, 2.02 Mt of intermediate products, and 3.34 Mt of primary nickel. Indonesia accounts for 1.9 Mt of the new intermediate capacity – comprising mixed hydroxide precipitate (MHP) from High Pressure Acid Leaching (HPAL) projects and matte produced from NPI conversion – and 1.95 Mt of new primary nickel capacity, including NPI, nickel cathode, and nickel sulphate. China P.R. represents 0.96 Mt of the new primary nickel capacity, mainly consisting of nickel cathode and nickel sulphate.

Nickel prices and stocks

Lastly, we will briefly analyse nickel prices and exchange stocks from the end of 2024 until October 2025.

The London Metal Exchange (LME) nickel price (close, cash seller) has trended lower since the beginning of 2023, falling from around 30,000 USD/t to levels converging close to 15,000 USD/t. After starting 2025 at 15,310 USD/t, prices peaked at 16,460 USD/t in mid-March, then fell sharply to a five-year low of 13,815 USD/t in early April. This drop coincided with a period of geopolitical uncertainty and unpredictability regarding international trade policies. After this trough in early April, prices recovered to a maximum of 15,725 USD/t in mid-May, coinciding with a weakening US dollar and the Indonesian Government’s announcement of higher royalties for raw materials. Since late May, prices have been moving in a narrowing band between 14,600 and 15,300 USD/t, ending October at 15,055 USD/t. During this period, there was a temporary tariff truce between China and the United States, that was renewed in August, news of loosening ore supply in Indonesia and a more stable, although lower, US dollar. Combined LME and Shanghai Futures Exchange (SHFE) end-of-month stocks increased from mid-2023 until March this year, when they totalled 231,000 t. Some small destocking occurred in April and May, followed by a brief period of subdued net deliveries through August. The upward trend then re-accelerated in September and October with a combined stock increase of over 50,000 t recorded across the two months. Total LME and SHFE stocks were 289,500 t by end-October, surpassing levels last seen in May 2018.

Chinese material has continued to strengthen its dominance in the composition of LME stocks. Between January and September, open tonnage of Chinese origin increased by 82,400 t, compared with a total net increase of 74,000 t across all countries. Consequently, China’s share grew from just under one-half (47%) to over two thirds (67.85%) over the period.

In contrast, material from Russia and Australia declined from 19% to 12.5%, and from 17% to 9.5%, respectively. Indonesia was the fourth-largest source of LME stocks, maintaining a share of just under 5% for most of the period and reaching 10,700 t by end-September, following net inflows of 3,700 t since the start of the year.

Nickel trading activity on the LME has recovered to levels above those seen before the disruption event in March 2022. Between January and October 2025, average daily volumes reached 86,700 contracts, surpassing the 68,700-contract average recorded over the same period in 2024 and the 68,000-contract average observed in 2021, prior to the 2022 trading suspension.

By the end of October, LME end-of-month off-warrant stocks had declined to 70,190 t, broadly in line with levels recorded at the end of 2024. This followed an increase to 82,338 t at the end of April, the highest level since reporting began in February 2020.

About this Tech Article

Appearing in the December 2025 issue of Stainless Steel World Magazine, this technical article is just one of many insightful articles we publish. Subscribe today to receive 10 issues a year, available monthly in print and digital formats. – SUBSCRIPTIONS TO OUR DIGITAL VERSION ARE NOW FREE.

Every week we share a new technical articles with our Stainless Steel community. Join us and let’s share your technical articles on Stainless Steel World online and in print.