It is arguably the most ambitious climate policy ever attempted, and one of the most complex. The European Union’s Carbon Border Adjustment Mechanism (CBAM) will reshape global trade by linking market access to carbon intensity. For stainless steel producers and importers, it represents both a regulatory challenge and a strategic turning point. For the past three years, CBAMBOO has supported companies across the value chain in getting ready for CBAM. Now, just days before the first financial liabilities, the mechanism is just around the corner – and key questions remain.

By Pauline Miquel, Policy & Research Lead, CBAMBOO

NOTE: This article originally appeared in December 2025, before the start of CBAM regulation.

CBAM: a new era for global trade

CBAM’s logic is simple: if European producers must pay for their carbon emissions through the EU Emissions Trading System (ETS), foreign producers should too. The goal is to prevent “carbon leakage” – when production moves to regions with weaker environmental rules – and to encourage global decarbonisation.

From January 2026, importers of stainless steel into the EU will need to monitor the embedded CO2 emissions in their goods and buy CBAM certificates matching verified values. Each certificate will reflect the ETS carbon price, which has fluctuated between EUR60 and EUR100 per tonne in recent years. For high-volume importers, this could mean multimillion-euro annual costs.

During the Transitional Period, running until the end of 2025, companies have been reporting quarterly on the emissions embedded in the products they import. This has forced importers to build new data-sharing practices with suppliers across complex global supply chains.

Carbon pricing at the border is expanding worldwide. The UK will introduce its own CBAM in 2027, followed by Norway, Taiwan and several other jurisdictions currently assessing feasibility. Paying for carbon will gradually become a new norm in international trade.

Transitioning from reporting to taxation: a confusing timeline

CBAM is the world’s first carbon border tax and one of the most ambitious climate instruments ever attempted.

Its rollout follows a two-phase design. The first phase – the Transitional Period – began in October 2023. During this stage, importers have been required to submit quarterly reports detailing embedded emissions from direct (Scope 1) and, in some cases, indirect (Scope 2) sources. These reports carry no financial obligations but have served as a testing ground for the system and an opportunity to build the necessary data infrastructure. The second phase will begin on 1 January 2026, marking the start of CBAM’s definitive regime. From that point, importers must purchase CBAM certificates corresponding to the embedded emissions in their goods. The price of these certificates will mirror that of allowances under the EU Emissions Trading System (ETS), introducing real financial exposure for importers.

Yet confusion has persisted throughout the Transitional Period. Supplier data quality remains uneven, and penalties for non-compliance have rarely been enforced. In early 2025, against a backdrop of geopolitical uncertainty, the European Commission announced several adjustments to streamline implementation. Most notably, CBAM will apply only to businesses importing more than 50 tonnes of covered goods—such as aluminium, steel, cement, hydrogen, and fertilisers – each year. This change removes over 90% of firms from the system while still capturing most of the embedded carbon.

A second adjustment delays the start of certificate purchases to February 2027. This means importers will transact up to a year after their goods enter the EU, easing the administrative burden in the early stages. The overlap between the two phases will nevertheless make early 2026 a particularly demanding period. Importers will need to submit their final Transitional Period report by 31 January 2026 for Q4 2025 imports, while also preparing for the financial and procedural requirements of the definitive regime. Certificates covering 2026 imports will be priced as the quarterly average of EU ETS prices, moving to weekly averages in 2027. This increased frequency is expected to improve market liquidity, allowing importers to monitor carbon prices more closely and manage volatility risks. To ensure compliance at customs, the Commission has introduced an importer authorisation system. Most companies should already have applied, though several national authorities only opened applications recently. The EU has therefore postponed the deadline to 31 March 2026. After that date, non-authorised importers will be unable to bring covered goods into the EU market.

The CBAM cost: a multi-variable formula

Less than two months before the hard start, the European Commission has yet to release key secondary legislation shaping the cost structure of the definitive regime. This lack of clarity adds uncertainty for importers in a low-margin, geopolitically exposed industry such as stainless steel.

Less than two months before the hard start, the European Commission has yet to release key secondary legislation shaping the cost structure of the definitive regime. This lack of clarity adds uncertainty for importers in a low-margin, geopolitically exposed industry such as stainless steel.

Understanding CBAM’s financial impact requires examining its phase-in structure. The mechanism will be introduced gradually as free ETS allocations to EU producers are phased out. The rate is set at 2.5% in 2026 and gradually increases until 2034.

Less than two months before the start of the definitive regime, the European Commission has yet to publish key secondary legislation defining CBAM’s cost structure. This delay adds uncertainty for importers, particularly in industries such as stainless steel where profit margins are thin and international exposure is high.

Assessing CBAM’s financial impact requires understanding how the mechanism will phase in over time. The policy will be introduced gradually, in parallel with the phase-out of free ETS allocations to EU producers. The CBAM factor begins at 2.5% in 2026 and will increase steadily until 2034.

However, this phase-in rate is only one part of the equation. Embedded emissions are the most decisive variable in determining liability. Importers can rely on default values—soon to

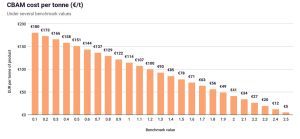

be published by the Commission—or collect verified data directly from suppliers. Default values will include a 20–30% punitive mark-up, creating a clear incentive to use actual data. Another key parameter is the benchmark, which defines the emission efficiency level at which CBAM costs begin to apply. Only the gap between EU best-in-class producers and foreign producers will be chargeable. Importers who can provide verified emissions data showing lower carbon intensity than the default values will therefore pay less.

If a producer’s home country already applies a comparable carbon price, importers may deduct those costs from their CBAM liability. In practice, however, most foreign carbon prices remain far below EU levels and are unlikely to have a significant impact in the near term.

Price volatility in the EU ETS adds further complexity. With carbon prices fluctuating between EUR60 and EUR100 per tonne in recent years, predicting future CBAM costs remains difficult. For high-volume importers, even small price movements can translate into major swings in financial exposure.

Even once all the details are finalised, CBAM’s complexity means importers may not know the precise cost of compliance until long after goods have cleared customs. To manage this uncertainty, companies will need robust internal systems that connect carbon data directly to procurement and pricing decisions.

What it means for stainless steel

Stainless steel is among the sectors most affected by CBAM. EU production relies entirely on scrap and low-carbon electricity, making it far more carbon-efficient than global averages. Under current rules, scrap counts as zero-emission material. The CBAM benchmark for EU-made stainless steel will therefore sit far below global levels. Strategic products imported to supply European manufacturers are often made via more carbon-intensive blast furnace routes. When compared against EU electricity-based production, the resulting CBAM cost could erase importers’ margins.

Stainless steel is among the sectors most affected by CBAM. EU production relies entirely on scrap and low-carbon electricity, making it far more carbon-efficient than global averages. Under current rules, scrap counts as zero-emission material. The CBAM benchmark for EU-made stainless steel will therefore sit far below global levels. Strategic products imported to supply European manufacturers are often made via more carbon-intensive blast furnace routes. When compared against EU electricity-based production, the resulting CBAM cost could erase importers’ margins.

For example, a company importing 10,000 tonnes of stainless-steel products at 2 tonnes of CO2e per tonne, with a carbon price of EUR 80, could face EUR 700,000 in annual CBAM costs. To address this, the European Commission will design benchmarks distinguishing between production routes. Importers sourcing from low-emission, EAF-based suppliers abroad will benefit if they can provide verified data. Without it, they will rely on higher-cost BF-based default values.

Default emissions will also be marked up by 30% in the definitive regime, creating a strong incentive to build supplier engagement and data-sharing systems. Many companies are already investing in digital tools to forecast CBAM exposure using their supplier data and benchmark scenarios such as those developed by CBAMBOO. In 2026, businesses that manage CBAM proactively will secure financial predictability, operational efficiency, and reputational leadership, turning proactive CBAM management into competitive advantage.

About the author

About the author

About the author

About the authorPauline Miquel is Policy & Research Lead at CBAMBOO. Her work focuses on monitoring regulatory evolutions across jurisdictions, external affairs, and public-facing content creation.

She holds a dual MSc in Environmental Economics and Climate Change from PKU and LSE, with research focused on CBAM implications for the steel industry. Previously, she worked as a Corporate Sustainability project manager in steel supply chains.

![]()

About this Featured Story

First appearing in the December 2025 issue of Stainless Steel World magazine, this Featured Story is just one of many insightful articles we publish. Subscribe today to receive 10 issues a year, available monthly in print and digital formats. – SUBSCRIPTIONS TO OUR DIGITAL VERSION ARE NOW FREE.

Every week we share a new Featured Story with our Stainless Steel community. Join us and let’s share your Featured Story on Stainless Steel World online and in print.